Artem has extensive experience in digital marketing, having worked with travel startups, Web3 games, and tech products. He helps us attract the right audience by combining in-depth market research with the internal expertise of the Ostride Labs team.

AUSTRAC Tranche 2: Five Architecture Risks FinTech Teams Miss

Updated 8 Feb 2026

()

A practical checklist for CTOs: where risks hide in real systems, and how to design controls that are easy to prove.

Most FinTech teams do not “ignore compliance”. They ship under delivery pressure, rely on certified vendors, and assume policies will cover the rest.

The problem is simpler: compliance architecture breaks in places that are invisible until an audit, a banking review, or an enterprise deal forces the question.

The good news: the highest-impact gaps are predictable and fixable. This article walks through five hidden risks that show up in AUSTRAC conversations, PCI DSS 4.0 assessments, and SOC 2 evidence cycles, plus the design moves that close them early.

Australian FinTech platforms face a compressed window into 2025-2026: PCI DSS 4.0 is already mandatory, and AUSTRAC Tranche 2 takes effect on 31 March 2026, expanding AML/CTF obligations across a much wider set of industries. If you support regulated onboarding, payments, wallets, cross-border transfers, or identity verification, you will be asked to prove controls, not just describe them.

TL;DR: Five hidden compliance risks you can fix early

If you are building or scaling a regulated FinTech product in Australia, these are the five architecture-level gaps that most often slow audits and enterprise deals:

Transaction monitoring at scale: systems that can’t adapt rules quarterly and process alerts within 72 hours create AUSTRAC exposure

Third-party vendor compliance: relying on vendor certifications without explicit controls creates liability gaps

Identity verification for ongoing risk: single-point onboarding checks miss UBO identification and risk-based escalation

Legacy system compliance debt: fragmented data and manual reporting prevent real-time compliance visibility

Executive oversight infrastructure: quarterly reporting without real-time dashboards creates personal liability for executives

Outcome:

You will know what to check, where the control must live in the system, and what to build so compliance does not become a delivery blocker.

If you want a fast read on your current exposure, we can review your compliance architecture and return a prioritised remediation plan.

Why Recent Enforcement Actions Matter

The enforcement landscape shifted dramatically in 2024-2025. AUSTRAC secured major penalties including SkyCity’s $67 million settlement and commenced proceedings against Entain Group (Ladbrokes/Neds) in December 2024. More critically, AUSTRAC announced they’d start targeting individual executives, not just entities.

The Privacy Act amendments introduced three-tier penalties reaching $50 million for serious breaches. Globally, transaction monitoring failures drove $3.3 billion in penalties, a 100% year-over-year increase.

Historical context shows the stakes: Westpac paid $1.3 billion (2020), Crown $450 million (2023), and these weren’t theoretical failures. They were systematic architecture gaps that compounded over time.

Risk 1: Transaction Monitoring That Can’t Keep Up

TD Bank paid $3.09 billion in 2024 for AML failures. The root cause? Their monitoring systems couldn’t process modern payment volumes, creating blind spots that enabled years of illicit activity.

Australian FinTech companies face identical risks at a smaller scale. Most transaction monitoring systems in SME stacks create gaps for 2025 regulatory requirements.

What’s Actually Broken

Your monitoring was probably built during rapid growth, designed to catch obvious patterns like structuring or round-number transfers. But sophisticated money laundering doesn’t work that way anymore.

Transaction monitoring failures now account for $3.3 billion in global penalties, a 100% year-over-year increase. Criminals evolve faster than detection systems.

Critical red flags:

Static rules not updated in 12+ months Modern money laundering shifts quarterly. Leading FinTech companies update monitoring rules quarterly (best practice), while 6 months is acceptable but risky. If your rules haven’t been updated in over 12 months, you’re in critical failure territory. Metro Bank got hit with £16 million in 2024 for failing to monitor 60 million transactions worth £51 billion because their systems couldn’t adapt.

Alert backlogs over 5 business days AUSTRAC’s 2024 priorities specifically flagged inadequate staffing for alert clearance as critical failure. If your team can’t triage alerts within 72 hours, you may be violating Section 41 of the AML/CTF Act.

No real-time detection for high-risk transactions Batch processing worked in 2015. With NPP handling instant transfers in 2025, delayed monitoring creates windows for criminals to move funds before detection.

Siloed data across payment channels If your system can’t correlate card payments, bank transfers, digital wallets, and international remittances, you have blind spots. 43% of suspicious matter report failures stem from fragmented architectures.

The Australian Context

AUSTRAC’s 2025 Rules introduced mandatory value transfer obligations (the “travel rule”) requiring comprehensive monitoring across all payment types. They’re targeting payment platforms and digital currency exchanges specifically.

Look at the December 2024 Entain Group enforcement (Ladbrokes, Neds). Key failures: inadequate controls for customer identity and source of funds, 24/7 digital platform without proper monitoring, board-level oversight failures.

For SME FinTech: your monitoring must be real-time, risk-based, and capable of handling actual transaction volumes without creating unmanageable backlogs.

What It Costs

Transaction monitoring failures carry $23 million max penalties per violation. But the real cost isn’t the fine. It’s the operational paralysis when AUSTRAC identifies systemic failures and issues remedial directions requiring expensive overhauls, independent audits, and enhanced reporting that runs 3-5x your original compliance budget.

Quick diagnostic:

Last monitoring rule review? (>6 months = acceptable but risky; >12 months = critical failure)

You outsourced payment processing for speed. Integrated white-label KYC because building in-house would take months. Rely on AWS or Azure because managing servers is expensive.

Here’s what you may not have considered: when your vendor has compliance failures, you’re still liable.

AUSTRAC’s 2024 guidance explicitly states “responsibility for compliance with AML/CTF obligations cannot be outsourced to third parties.” Yet vendor failures now represent a primary vector for compliance breaches across FinTech.

The Vendor Risk Architecture

Modern FinTech stacks are built on third-party integrations. Payment gateways, identity verification, fraud detection APIs, cloud infrastructure, communication platforms. Each one introduces compliance obligations and potential failure points.

The risk compounds because most SME companies don’t have formal vendor compliance verification. You review marketing materials, check their SOC 2 report (if you’re disciplined), start integrating. But SOC 2 doesn’t cover AUSTRAC compliance. ISO 27001 doesn’t guarantee Privacy Act adherence.

Danger signals:

No documented vendor due diligence If you can’t produce written assessments of each vendor’s compliance capabilities, data handling, and regulatory alignment, you may be operating with gaps.

Vendors handling regulated data without explicit agreements Your payment processor has transaction data. Your KYC provider stores identity documents. Your CRM has personal information. If contracts don’t explicitly define compliance responsibilities, data retention, breach notification, and audit rights, you may be exposed.

Shadow data you can’t access 82% of breaches involve cloud-stored data, with significant portions in “shadow data” repositories. Information stored by vendors outside your visibility and control. Under Privacy Act 2024, you’re liable for vendor data handling even if you can’t see it.

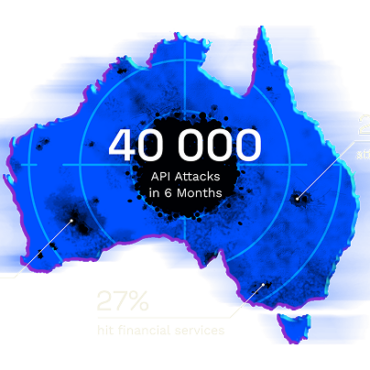

API integrations without security assessment 95% of organisations experienced API security incidents within 12 months. Malicious API traffic grew 681%. Every vendor API creates potential compliance vulnerabilities if not properly secured.

Australian Requirements

Privacy Act 2024 amendments introduced a “whitelist” mechanism for overseas data transfers. You must ensure recipient countries provide substantially similar privacy protections. For FinTech using global vendors (common for payments, fraud detection, infrastructure), this creates complex compliance mapping.

The $80 Million Lesson

In January 2025, Block Inc. (Cash App) settled with 48 U.S. state regulators, paying $80 million for AML compliance failures. Core issues? Inadequate customer due diligence, failure to implement sufficient risk-based controls for high-risk accounts, and inadequate transaction monitoring across more than 50 million users.

Block cooperated with regulators and agreed to hire an independent consultant to review their entire BSA/AML program. But the damage was done. For a platform processing billions in transactions annually, these compliance gaps created systematic exposure to money laundering and terrorism financing risks.

The parallel for Australian FinTech: your vendors must demonstrate actual compliance capability, not just certifications.

Quick diagnostic:

Do you have written vendor compliance assessments? (Required for audit defense)

Can vendors provide breach notifications within 24-72 hours? (Privacy Act expectation)

Can you audit vendor systems for your data? (Essential for liability management)

Risk 3: Identity Verification Built for Speed, Not Security

Speed matters in onboarding. Every additional second of friction costs conversions. But verification systems optimized purely for speed create systematic compliance exposure.

SkyCity paid $67 million for CDD failures across 329 contraventions. The pattern: verification processes that prioritized customer experience over regulatory requirements.

The Onboarding Trap

Most FinTech platforms verify identity once at account opening. Automated document checks, maybe selfie verification, quick approval. But AUSTRAC requirements extend far beyond initial identity verification.

Critical gaps in standard onboarding:

Single verification at account opening, no ongoing monitoring Customer risk profiles change. Initial low-risk customers may engage in activities triggering enhanced due diligence requirements. If you’re not monitoring for risk escalation triggers, you miss regulatory obligations.

Can’t identify Ultimate Beneficial Owners (UBOs) For business accounts, you need to identify individuals with 25%+ ownership or control. Many platforms capture business registration but don’t verify UBO identity. AUSTRAC requires this for all business customers.

No risk-based escalation for high-risk profiles Politically exposed persons (PEPs), customers from high-risk jurisdictions, unusual transaction patterns should trigger enhanced CDD automatically. If your system doesn’t flag and escalate these, you have blind spots.

Source of funds verification limited or absent For deposits over $10,000 or customers flagged as high-risk, source of funds verification is required. If your onboarding workflow doesn’t support this, compliance teams must work around the system, creating documentation gaps.

The Australian Reality

Crown Melbourne and Crown Perth paid $450 million across 329 CDD contraventions. The failures weren’t theoretical. They were systematic gaps in how customer relationships were verified and monitored.

For SME FinTech, the requirement is the same: you need systems that support risk-based verification, not just one-size-fits-all onboarding.

Quick diagnostic:

Can you identify UBOs for all business accounts? (AUSTRAC requirement)

Does your system automatically flag high-risk profiles for enhanced checks? (Risk-based approach)

Can you verify source of funds for large deposits? (Required for suspicious activity assessment)

Do you conduct ongoing customer due diligence reviews? (Not just onboarding)

Risk 4: Legacy Systems as Compliance Time Bombs

Your original architecture made sense when you had 1,000 customers and processed $1 million monthly. At 50,000 customers and $50 million monthly volume, those same systems create systematic compliance exposure.

TD Bank’s $3.09 billion penalty stemmed largely from legacy systems that couldn’t handle modern payment volumes. Between 2018 and 2024, 92% of their transactions went unmonitored because systems weren’t updated to handle scale.

Technical Debt Becomes Compliance Debt

The warning signs that technical debt has become compliance debt:

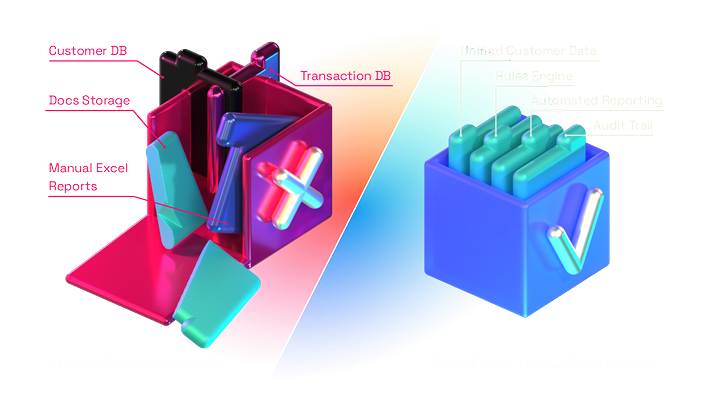

Data scattered across multiple systems without unified view Customer data in one database, transaction history in another, compliance documentation in a third. When auditors ask for complete customer activity records, you need days or weeks to compile. AUSTRAC expects real-time or near-real-time access.

Manual processes for regulatory reporting If generating SMRs, TTRs, or IFTIs requires manual data extraction and Excel manipulation, you introduce errors and delays. Errors in reporting carry penalties. Delays in SMR filing (>3 business days) violate Section 41.

No comprehensive audit trail Privacy Act 2024 explicitly requires “technical and organisational measures” for data protection. If you can’t produce tamper-proof audit logs showing who accessed what data when, you create exposure in data breach scenarios.

Can’t make configuration changes without code deployments Compliance rules change. AUSTRAC issues new guidance. If updating monitoring rules or verification workflows requires full development cycles, you’re structurally behind regulatory evolution.

The Architecture Pattern That Works

Platforms that maintain compliance at scale have common architecture patterns:

Unified customer data model:

Single source of truth for customer information, accessible across compliance, operations, and reporting functions.

Configurable rules engine:

Business users can update monitoring rules, verification workflows, and risk scoring without engineering deployment.

Automated regulatory reporting:

SMRs, TTRs, IFTIs generated automatically from transaction data, with manual review before submission but no manual compilation.

Comprehensive audit logging:

Every data access, every configuration change, every compliance decision logged with timestamp and user identity, immutable storage for 7+ years.

Quick diagnostic:

Can you generate a complete customer activity report in under 5 minutes? (Unified data requirement)

Are SMRs/TTRs/IFTIs generated automatically? (Reduces error risk)

Do you have tamper-proof audit logs with 7-year retention? (Privacy Act requirement)

Can the compliance team update rules without engineering? (Agility requirement)

Risk 5: Executive Oversight Gaps Create Personal Liability

AUSTRAC’s 2024 enforcement shift: they’re now joining individual executives to proceedings, not just pursuing entities.

Star Entertainment’s former Chief Casino Officer paid $180,000 personally and received an 18-month director disqualification. Former CFO: $60,000 and 9-month disqualification. These were not criminal charges. These were civil penalties for failing to exercise reasonable care and diligence in their duties.

The Governance Gap

Board and executive oversight of compliance typically happens quarterly through written reports. For rapidly evolving compliance risks, quarterly reporting creates dangerous blind spots.

Red flags in governance infrastructure:

Quarterly or annual compliance reporting only Compliance risks evolve faster than quarterly board cycles. If executives only see compliance metrics every 90 days, they can’t respond to emerging issues in time.

No real-time compliance dashboard for executives If the CEO or CFO needs to request reports to see current alert backlogs, SMR filing status, or vendor compliance posture, they lack visibility needed to exercise oversight.

Inadequate documentation of risk-based decisions When you accept compliance risks (accepting certain customers, delaying controls implementation), documentation of the risk assessment and acceptance rationale protects executives. Without it, risk acceptance looks like negligence.

Insufficient compliance resources relative to scale Benchmark: 1 dedicated compliance FTE per $50 million monthly transaction volume. Below this, you may not have adequate resources to maintain programme effectiveness, creating systematic rather than isolated failures.

What “Personal Liability” Actually Means

The Star Entertainment penalties demonstrate the standard: executives are expected to actively oversee compliance, not just rely on compliance team reports.

This means:

Asking probing questions about compliance program effectiveness

Understanding key compliance metrics and what they indicate

Ensuring adequate resources for compliance function

Documenting risk-based decisions with clear rationale

It doesn’t mean executives need to be compliance experts. It means they need systems that give them visibility and documentation practices that demonstrate active oversight.

Quick diagnostic:

Does your board receive monthly compliance reports? (Quarterly may be insufficient)

Can executives access real-time compliance dashboard? (Visibility requirement)

Are risk acceptance decisions documented with rationale? (Liability protection)

Do you have adequate compliance staffing? (1 FTE per $50M monthly volume benchmark)

30-Day Compliance Architecture Audit

If you’ve identified gaps through the diagnostics above, here’s a structured 30-day assessment approach:

Week 1: Discovery and Documentation

Days 1-3: System Inventory Document all systems handling customer data, transaction data, or compliance workflows. Map data flows between systems. Identify manual processes and workarounds. Create an architecture diagram showing where customer data exists.

Days 4-7: Transaction Monitoring Assessment Review current monitoring rules and last update date. Analyze alert backlogs and processing times. Test cross-product correlation capabilities. Document gaps in real-time detection for high-risk transactions.

Week 2: Risk Assessment

Days 8-10: Vendor Compliance Review List all vendors handling regulated data. Review vendor contracts for compliance provisions. Verify vendor certifications and their scope. Identify shadow data and overseas transfer compliance. Document gaps in vendor due diligence.

Days 11-12: Identity Verification Review Evaluate customer onboarding flows: verification methods, risk-based CDD triggers, ongoing monitoring, UBO identification for business accounts. Test whether high-risk scenarios trigger appropriate enhanced due diligence automatically.

Days 13-14: Governance Infrastructure Review board and management reporting: frequency, content, real-time availability, documentation of risk-based decisions. Assess whether compliance functions have adequate authority, resources, and independence.

Week 3: Remediation Planning

Days 15-17: Technical Roadmap Prioritise architectural improvements: consolidated data views, automated reporting, audit trail enhancements, monitoring rule updates, API security hardening. Map dependencies and sequence work to address highest-risk gaps first while minimising operational disruption.

Days 18-19: Vendor Management Framework Design standardised vendor assessment: due diligence requirements, contract templates with compliance provisions, ongoing monitoring, breach response protocols. Begin implementing with highest-risk vendors first.

Days 20-21: Governance Enhancement Design executive compliance dashboard: key metrics, real-time visibility requirements, escalation triggers, board reporting cadence. Document risk-based decision-making frameworks and create templates for compliance committee minutes demonstrating active oversight.

Days 25-27: Stakeholder Communication Brief board and senior management on assessment findings, risk priorities, remediation plan. Conduct compliance training for relevant staff on enhanced procedures. Establish clear accountability for remediation work streams.

Days 28-30: Ongoing Monitoring Implement tracking for remediation progress, compliance metrics, emerging regulatory developments. Establish quarterly compliance assessment cadence for continuous improvement and adaptation to evolving requirements.

Why Prevention Beats Remediation

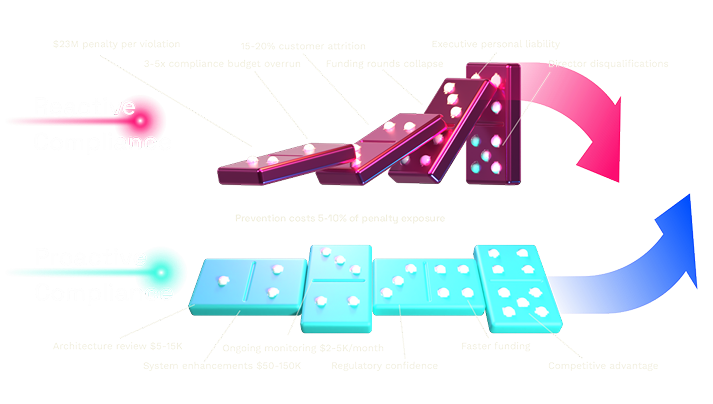

Financial penalties are staggering: $1.3 billion Westpac, $450 million Crown, $67 million SkyCity. But for SME FinTech, the real cost isn’t the penalty. It’s operational paralysis, reputational damage, executive liability accompanying enforcement actions.

When AUSTRAC issues remedial directions, companies typically spend 3-5x their original compliance budget on remediation, independent audits, enhanced reporting, system overhauls. Customer attrition during compliance reviews averages 15-20% as legitimate customers get caught in tightened controls. Funding rounds collapse when investors discover systematic compliance gaps. Executive teams face personal liability and career-ending director disqualifications.

For SME FinTech, prevention isn’t just cheaper than remediation. It’s strategically essential. Companies building compliance into architecture from day one move faster, raise capital more easily, withstand regulatory scrutiny that destroys unprepared competitors.

Moving From Risk Assessment to Regulatory Confidence

These five hidden compliance risks aren’t edge cases. They’re systematic vulnerabilities embedded in most SME FinTech platform architectures.

Companies that survive and thrive in Australia’s increasingly stringent regulatory environment aren’t necessarily those with the biggest compliance budgets. They’re companies treating compliance as an architectural requirement from day one, building systems that scale with transaction volumes and regulatory complexity, maintaining governance infrastructure demonstrating active board and management oversight.

For CTO decision-makers at SME FinTech companies, the path forward requires three strategic shifts:

Shift compliance left in development

Stop treating compliance as a gate after features are built. Design compliance capabilities into architecture: audit trails, data consolidation, automated reporting, risk-based workflows. Compliance-by-design reduces retrofitting costs by 60-80% compared to post-launch remediation.

Invest in visibility and observability

You can’t manage what you can’t measure. Real-time compliance dashboards, comprehensive audit trails, automated reporting aren’t optional. They’re a minimum viable infrastructure for demonstrating programme effectiveness to regulators and protecting executives from personal liability.

Build vendor management into procurement

Every vendor integration is a compliance decision. Implement standardised due diligence, explicit compliance provisions in contracts, ongoing monitoring of vendor compliance posture. Proper vendor management costs 5-10% of potential exposure from vendor failures.

The regulatory environment will only intensify. AUSTRAC’s enhanced enforcement, Privacy Act penalties reaching $50 million, willingness to pursue individual executives create unprecedented risk for under-prepared companies. But these same regulations create competitive advantages for companies building compliance capabilities that scale.

Transform Your Compliance Architecture

The diagnostic framework in this article identifies risks. Addressing them requires systematic remediation balancing compliance requirements with operational realities and growth objectives.

Book a Free Compliance Architecture Review – our team assesses your tech stack, identifies critical gaps, provides a prioritised remediation roadmap tailored to your risk profile and transaction volumes. Unlike generic compliance audits, we focus specifically on technical and architectural vulnerabilities triggering AUSTRAC enforcement actions.

Case studies and enforcement examples cited are based on publicly available regulatory filings and media reports. Penalty amounts and enforcement details are accurate as of publication date but may be subject to ongoing legal proceedings. This article provides general information and technical guidance but does not constitute legal advice. Australian FinTech companies should consult qualified legal counsel for specific compliance questions.

Ostride Labs – We build products with full compliance confidence. Australian-focused compliance engineering for FinTech, RegTech, and EdTech companies that need to ship fast without creating regulatory liability.

Rating:

Share

Our newsletter (you’ll love it):

Let's talk!

Enter your data below to instantly download the checklist.

Book a free 30-minute scaling assessment with our experts.

Cloud Security DevOps Engineer

Full time

Requirements

5+ of experience working with public or private cloud components, administration, and support

3+ years and expert-level skills working in a SRE role involving at least two of these cloud providers: GCP, MS Azure or AWS

Experience setting up, adjusting, and administering monitoring tools, including alarm configurations and log level analysis

Ability to learn applications functionally and technically, and work on troubleshooting with minimal input from the application team

Experience automating routine procedures

Experience and the ability to elaborate on success stories of increasing fault-tolerance of multi-datacenter infrastructure

Excellent Linux/Unix administration skills and deep understanding of Linux OS principles

Knowledge of bash, network protocols, and implementation principles for major cloud providers

Excellent theoretical knowledge of the OpenShift Container platform and its low level features and limitations

Site Reliability Engineer

Full time

Requirements

5+ of experience working with public or private cloud components, administration, and support

3+ years and expert-level skills working in a SRE role involving at least two of these cloud providers: GCP, MS Azure or AWS

Experience setting up, adjusting, and administering monitoring tools, including alarm configurations and log level analysis

Ability to learn applications functionally and technically, and work on troubleshooting with minimal input from the application team

Experience automating routine procedures

Experience and the ability to elaborate on success stories of increasing fault-tolerance of multi-datacenter infrastructure

Excellent Linux/Unix administration skills and deep understanding of Linux OS principles

Knowledge of bash, network protocols, and implementation principles for major cloud providers

Excellent theoretical knowledge of the OpenShift Container platform and its low level features and limitations

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.